Value Added Tax

VAT, also known as Value Added Tax, is a tax that is levied on the consumer. The responsibility of collecting this tax lies with the business, who then pays it to the relevant tax authority. In the United Kingdom, this authority is HM Revenue & Custom ( https://www.gov.uk/government/organisations/hm-revenue-customs ), while in Belgium it is the Service Public Federal Finance (https://finance.belgium.be/en/npo). Similarly, in the Kingdom of the Netherlands, the tax and customs administration, known as Belastingdienst (https://www.belastingdienst.nl/ ), is responsible for collecting VAT. In the United Arab Emirates, it is the Ministry of Finance (https://mof.gov.ae/vat/) that holds the authority over taxation. These organizations ensure that VAT is collected and used for the appropriate purposes, contributing to the overall financial stability and growth of their respective countries.

VAT, or Value Added Tax, is a tax that is added to the price of most products and services sold by businesses that are registered for VAT. The amount of VAT that you pay is generally the difference between the VAT that you have paid to other businesses and the VAT that you have charged to your customers. If you have charged more VAT than you have paid, you will need to pay the difference to the Tax authority. This occurs when your vatable sales exceed your vatable purchases and expenses. On the other hand, if you have paid more VAT than you have charged, the Tax authority will typically reimburse you the difference. This happens when your vatable sales are lower than your vatable purchases and expenses.

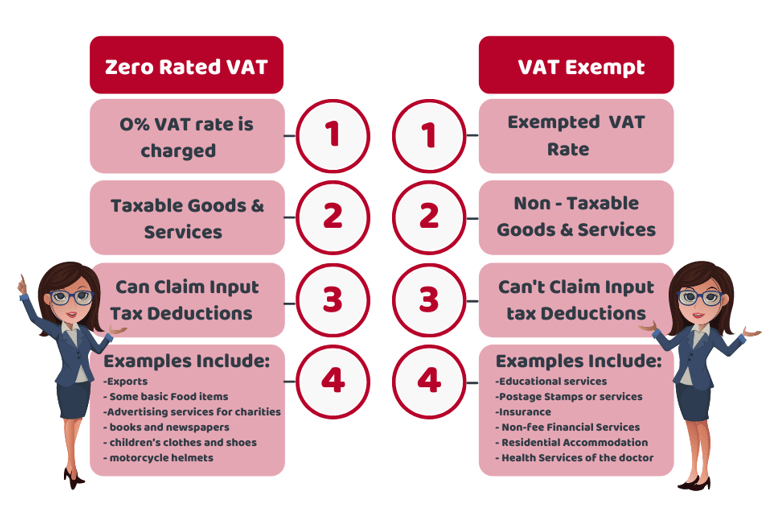

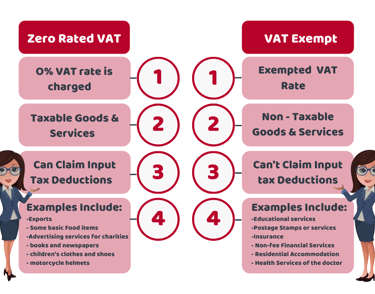

VAT, or Value Added Tax, is levied on the sale of both goods and services, depending on the specific requirements of the consumer. However, it is important to note that certain essential goods, such as basic food items, are exempted from VAT in order to alleviate the burden on consumers. Similarly, services related to healthcare and care are also exempt from VAT. This ensures that individuals receive necessary goods and services without the additional cost of VAT.

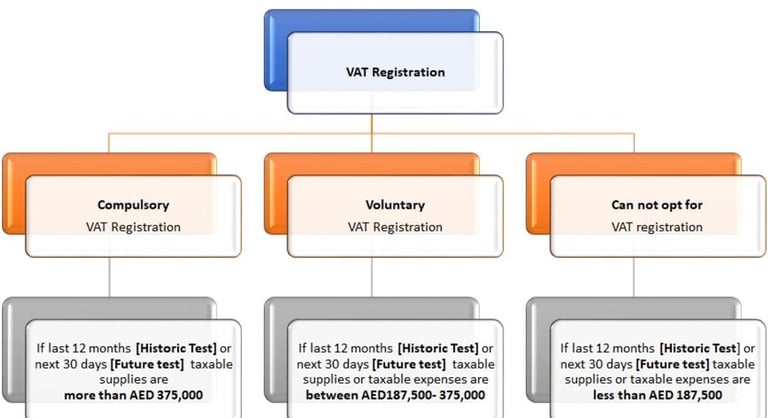

VAT threshold for Registration:

Many countries have different rules regarding VAT thresholds. In the UK, if a business's total VAT taxable turnover for the last 12 months was over £85,000 (the VAT threshold), or if the business expects its turnover to exceed £85,000 in the next 30 days, it must register for VAT.

The European Union has called on its member states to provide a VAT threshold for local businesses. In Belgium, a business is required to register for VAT if its annual turnover exceeds €25000 and if it is engaged in the supply of goods or services as defined in the Belgian VAT Code. This means that both Belgian and non-Belgian businesses are subject to VAT obligations in Belgium under certain circumstances. It is important for businesses operating in Belgium to familiarize themselves with the Belgian VAT Code and understand their VAT obligations in order to comply with the law. The EU's push for member states to offer a VAT threshold aims to provide support and flexibility for small businesses, allowing them to operate more efficiently and effectively within the EU market.

There is no VAT registration threshold for non-resident companies providing taxable supplies in Belgium. However, foreign companies selling goods to Belgian consumers via the internet have a €35,000 per annum threshold. This means that if a foreign company exceeds this threshold, it is required to register for VAT in Belgium and charge VAT on its sales to Belgian consumers. This threshold is specifically applicable to online sales and is aimed at ensuring that foreign companies selling goods online to Belgian consumers are also subject to the same tax obligations as Belgian companies. It is important for foreign companies to be aware of this threshold and comply with the VAT registration requirements to avoid any penalties or legal consequences.

For foreign businesses trading in the Netherlands and registered for VAT/GST/Tax in their home state, there is no VAT registration threshold. However, for EU VAT registered companies that sell goods online to consumers in the Netherlands, the VAT registration threshold (known as distance selling) is €100,000 per year. This means that if a company's annual sales to Dutch consumers exceed €100,000, they must register for VAT in the Netherlands. This threshold is in place to ensure that companies that generate significant revenue from selling to Dutch consumers contribute their fair share of VAT. It is important for foreign businesses to understand and comply with these regulations to avoid any penalties or legal issues related to VAT registration and collection in the Netherlands.

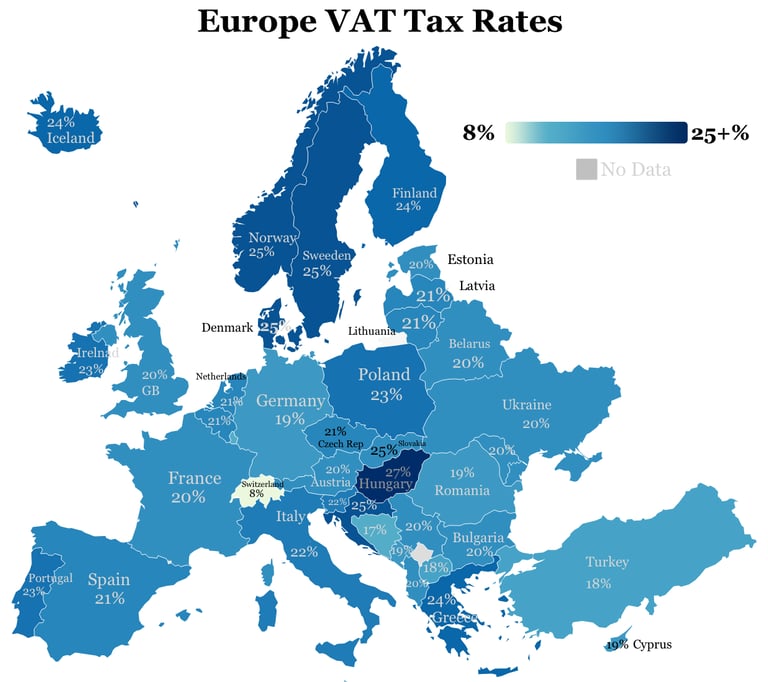

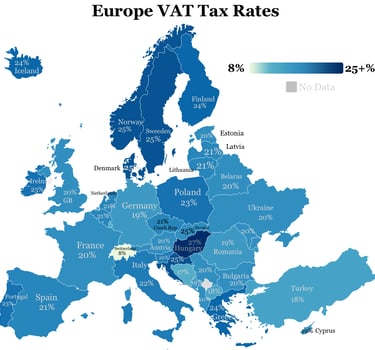

VAT Rates

The standard rate for VAT in the UK is 20%, in Belgium and the Netherlands it is 21%, and in the UAE it is 5%. The term used for Value Added Tax in the local language differs among these countries. In Dutch, it is known as "Belasting over de Toegevoegde Waarde" or BTW, while in French it is referred to as "Taxe sur la Valeur Ajoutée" or TVA. These terms are used to describe the same type of tax, which is applied to the value added at each stage of production and distribution. VAT rates vary among countries and can have a significant impact on the cost of goods and services.

The standard rates for Value Added Tax (VAT) vary across different countries. In the United Kingdom, the standard rate is 20%, while Belgium and the Netherlands have a standard rate of 21%. The United Arab Emirates (UAE) has a lower standard rate of 5%. In Dutch, VAT is referred to as "Belasting over de Toegevoegde Waarde" (BTW), and in French, it is called "Taxe sur la Valeur Ajoutée" (TVA). Among European countries, Luxembourg has the lowest standard VAT rate at 16%, followed by Malta at 18%. Cyprus, Germany, and Romania all have a standard VAT rate of 19%. These variations in VAT rates reflect the different tax policies and economic conditions of each country.

VAT for online Business

Amazone, Ebay, and other websites are online platforms used for selling goods or services. These websites can be operated from anywhere, but the application of Value Added Tax (VAT) depends on the location of the sale and the customers. For instance, if a business is registered in Europe and has customers in the UK, but ships the goods from Europe, the point of sale is considered to be in Europe. However, if a company based in the EU sells goods to customers and ships the products from the UK, the business will need to charge UK customers VAT. In this case, the business should also be registered for UK VAT with HM Revenue & Customs. In the UK, this process is known as online or distance selling. (source: https://www.gov.uk/online-and-distance-selling-for-businesses)

One Stop Shop (OSS)

The One Stop Shop (OSS) is an electronic portal that allows online sellers to simplify their VAT registration process. Instead of registering for VAT in every EU Member State (MS) where they supply goods, sellers can use the OSS to account for and pay VAT in all EU MS on a single quarterly return in one EU MS. This streamlined system helps businesses save time and resources by eliminating the need for multiple registrations. In order to be eligible for the OSS, the annual threshold is set at 10000 Euro. By utilizing this convenient platform, online retailers can efficiently manage their VAT obligations across the European Union.

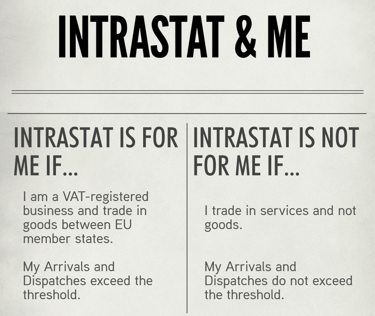

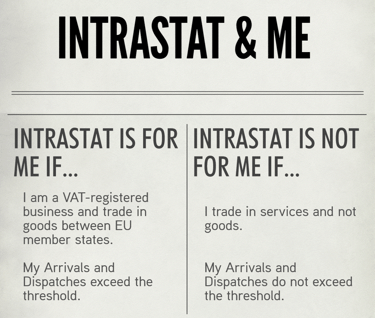

Intrastaat

Intrastat reporting is a requirement for businesses involved in the movement of goods within EU member states. This reporting obligation applies only to goods and excludes services. Companies engaged in international trade across the European Union may have to comply with additional reporting requirements in addition to filing periodic VAT returns and European Sales Listings (ESL). Intrastat reporting is necessary for companies that exceed the reporting thresholds in the countries they trade with. It is a system designed to collect statistics on the trade in goods between Northern Ireland and EU member states.

If a business in the UK is registered for VAT and sends goods worth £250,000 from Northern Ireland to EU member states, or receives goods worth £500,000 in Northern Ireland from EU member states that exceed a legally set threshold, it is mandatory to provide information about the movement. This information is submitted electronically using a form called an Intrastat Supplementary Declaration (SD). However, businesses that are not registered for VAT and individuals who transport goods between Northern Ireland and the EU are not required to comply with the intrastat system.

Frequently Ask Questions

An EU business can sell its products to another EU-VAT registered business operating in a different EU country without charging VAT on the sale. However, if the same product is sold to a final consumer within the EU, the business may be required to charge VAT at the applicable rate in their own country. To simplify the VAT process, the business has the option to register for the One Stop Shop in their local member state. This allows them to report and pay VAT for their cross-border sales in a centralized manner, eliminating the need to register and file VAT returns in each individual country where they make sales. The One Stop Shop system helps businesses save time and resources while ensuring compliance with EU VAT regulations. (Source: https://europa.eu/youreurope/business/taxation/vat/cross-border-vat/index_en.htm#outsidetheeu)

An EU business can sell goods to customers outside the EU without charging VAT. This means that customers in countries outside the EU can purchase goods from the EU business at a lower cost, as they do not have to pay the VAT tax. This can be beneficial for both the EU business and the customers, as it allows for increased sales and more competitive pricing. However, it is important for the EU business to properly document and track these sales to ensure compliance with tax regulations. By not charging VAT, the EU business can attract a larger customer base and potentially expand its reach into international markets.

EU based companies that are selling goods or services to EU customers are required to use the One-Stop Shop (OSS) system. This means that they can collaborate with the tax administration of their own Member State and register their business in a single member state of the EU. By doing so, these companies can streamline their operations and comply with the necessary tax regulations. The OSS system provides a centralized platform for reporting and paying VAT, making it easier for businesses to manage their cross-border transactions within the EU. This efficient and simplified process promotes trade and ensures that companies meet their tax obligations in a seamless manner.

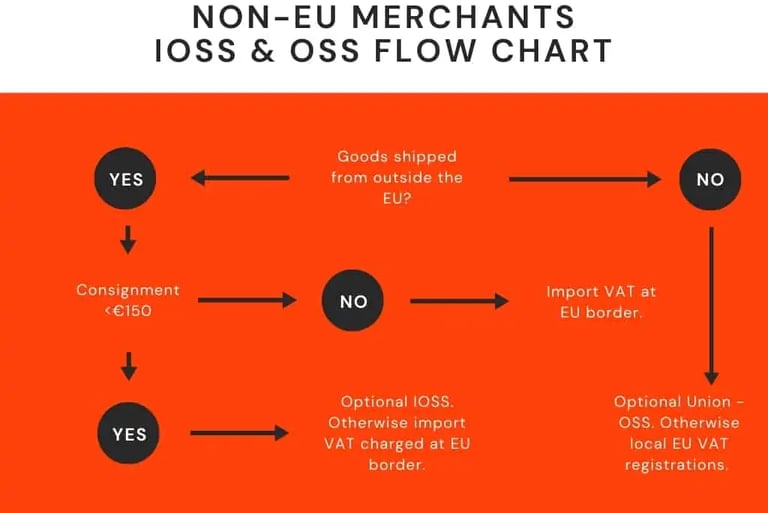

Non-EU companies selling goods valued less than €150 to EU customers can benefit from the Import One Stop Shop (IOSS). This system allows businesses to avoid the need to register for VAT in each individual EU member state. Additionally, goods sold under the IOSS are exempt from excise duties, which are indirect taxes applied to specific products such as alcohol or tobacco. By utilizing the IOSS, non-EU companies can streamline their operations and simplify their tax obligations when selling to EU customers. This ensures a smoother and more efficient process for both the businesses and their customers, ultimately facilitating cross-border trade within the EU.

If a UK VAT registered business sells, sends, or transfers goods out of the UK, they typically do not need to apply VAT to those transactions. This means that the business can sell their products or goods to customers located outside of the UK without including VAT in the price. This exemption from charging VAT on exports allows UK businesses to remain competitive in the global market and encourages international trade. However, it is important for the business to maintain proper records and documentation to substantiate the export of goods and comply with any relevant customs regulations. It is advisable for businesses to seek professional advice or consult with tax authorities to ensure they are correctly applying the VAT rules for international transactions.

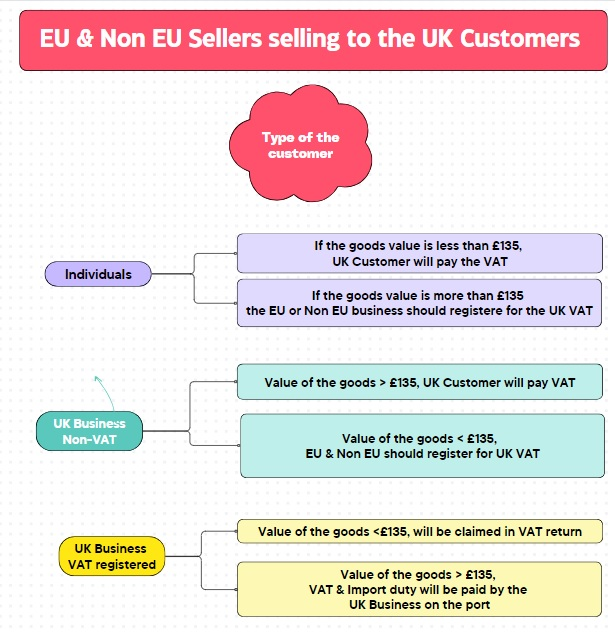

If the business is an overseas seller with goods located in the UK at the time of sale, they are required to register and account for VAT on all sales made directly to customers in Great Britain or Northern Ireland. This means that regardless of the value of the goods, the business must comply with VAT regulations and properly calculate and report the appropriate taxes. This ensures that the business is operating legally and fulfilling its obligations to the tax authorities. It is important for overseas sellers to understand and adhere to these requirements in order to avoid any penalties or legal issues. By registering and accounting for VAT, the business can confidently conduct sales in the UK market and maintain a good standing with customers and authorities.

Foreign companies can now register for VAT in the UK without the requirement of establishing a local company. This practice, known as non-resident VAT trading, allows foreign companies to conduct taxable supplies in the UK. However, it is important to note that there is no longer a non-resident VAT registration threshold. Therefore, foreign companies providing taxable supplies must register for UK VAT immediately. This change in regulations facilitates foreign companies' participation in the UK market, enabling them to engage in business activities and comply with the necessary taxation requirements.

Types of VAT Scheme in the UK

There are various VAT schemes available to cater to a business specific requirements, each with its own eligibility criteria and reporting obligations. The most commonly used schemes are as follows:

Standard VAT accounting scheme: This scheme is designed to use the standard VAT rate and is dependent on the tax point indicated on the invoice, whether it is a sale invoice, purchase invoice, or expense invoice. The VAT amount on purchases and expenses is deducted from the VAT amount on sales.

VAT Flat Rate Scheme: This scheme is designed to use the discounted VAT rate only on the sale. VAT on purchase can not be claimed, but can be claimed on assets having value for more than £2000. The sale excluding VAT should be less than £150,000 per year, to be eligible for this scheme.

VAT Cash Accounting Scheme: This scheme is for the small business, who's turnover is less than £1.6m , use Standard VAT rate, but calculation is based on money in and out (receipt or payment) and not on the invoice date.

VAT Annual Accounting Scheme: If a business has turnover less than £1.6m, can opt for this scheme, to file VAT return annually, however, payments will be made either quarterly or by 9 instalments in advance.

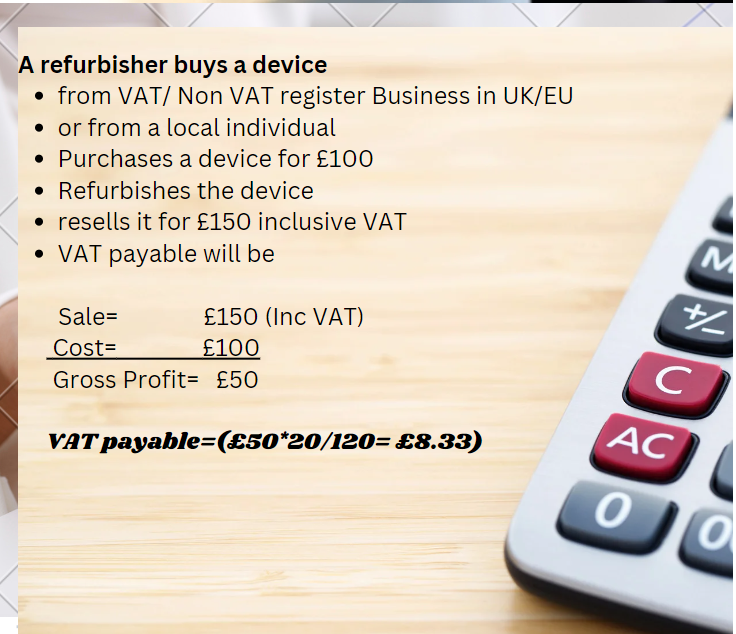

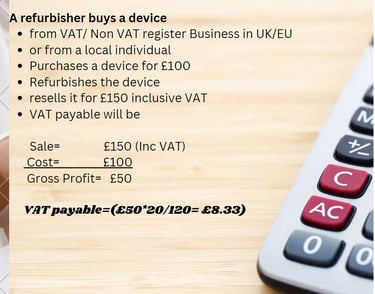

VAT margin schemes: A business involve in selling second hand items, use this scheme. Under this scheme, VAT is charged with standard rate on the gross profit of the second hand items. A business buys goods from a wholesaler in the UK or EU, the wholesaler will invoice the business with zero vat in the invoice.